Predictions (2024)

Prediction

Quote

Status

Remote work is expected to become more widely accepted and offer more flexible roles compared to traditional employment.

The acceptance of remote work is becoming significantly better than being in a job. The flexible roles it brings are wonderful.

1 year ago

Correct

Remote work is expected to become more widely accepted and offer more flexible roles compared to traditional employment.

The acceptance of remote work is becoming significantly better than being in a job. The flexible roles it brings are wonderful.

Correct

Given Shubham's home loan and potential benefits from deductions like ELSS, the old tax regime might still be more advantageous for him than the new one.

My actual salary which I told is 67 K in hand, in this sir, my TDS of Rs 4 K is deducted per month, which I file sir, then I will get it back, so if I put my money in then it can happen because if you have a home loan, you get its benefit and if you do EIL then you get its benefit, so it is possible that the old tax regime is still beneficial for you and if So please continue with ELSS. If not, you can stop ELSS and move to the new tax regime.

1 year ago

Correct

Given Shubham's home loan and potential benefits from deductions like ELSS, the old tax regime might still be more advantageous for him than the new one.

My actual salary which I told is 67 K in hand, in this sir, my TDS of Rs 4 K is deducted per month, which I file sir, then I will get it back, so if I put my money in then it can happen because if you have a home loan, you get its benefit and if you do EIL then you get its benefit, so it is possible that the old tax regime is still beneficial for you and if So please continue with ELSS. If not, you can stop ELSS and move to the new tax regime.

Correct

When making prepayments on loans, Shubham should prioritize reducing the loan tenure over lowering the EMI to save on interest.

But if you tell them that you will take this 5,000 rupees and reduce my tenure, not my EMI, then this is a big mistake. People make when they make a prepayment, the bank says, 'Sir, reduce the EMI.' And we all reduce the EMI. Why? Because we like reducing the EMI. We feel that we have saved money every month, but because of that, you are still paying the loan for 15 years.

1 year ago

Correct

When making prepayments on loans, Shubham should prioritize reducing the loan tenure over lowering the EMI to save on interest.

But if you tell them that you will take this 5,000 rupees and reduce my tenure, not my EMI, then this is a big mistake. People make when they make a prepayment, the bank says, 'Sir, reduce the EMI.' And we all reduce the EMI. Why? Because we like reducing the EMI. We feel that we have saved money every month, but because of that, you are still paying the loan for 15 years.

Correct

An FD-backed credit card can be considered to build credit score, by opening a fixed deposit and using the credit card responsibly with regular monthly payments.

if you ever want to consider it is an FD backed credit card then you open a fixed deposit with a bank against which you will get a credit limit and if you start using that credit card properly where you are making regular monthly payments etc you will then build your credit score

1 year ago

Correct

An FD-backed credit card can be considered to build credit score, by opening a fixed deposit and using the credit card responsibly with regular monthly payments.

if you ever want to consider it is an FD backed credit card then you open a fixed deposit with a bank against which you will get a credit limit and if you start using that credit card properly where you are making regular monthly payments etc you will then build your credit score

Correct

When needing to withdraw funds, select assets with the least variability, such as large-cap mutual funds, to mitigate the risk of selling at a loss during market downturns.

always withdraw from the least variable asset i.e. liquidate such an investment in which wallet or variability is the least in your case it will be mostly the large cap mutual fund from mid cap and small cap If you do this, it is possible that the market may go down.

1 year ago

Correct

When needing to withdraw funds, select assets with the least variability, such as large-cap mutual funds, to mitigate the risk of selling at a loss during market downturns.

always withdraw from the least variable asset i.e. liquidate such an investment in which wallet or variability is the least in your case it will be mostly the large cap mutual fund from mid cap and small cap If you do this, it is possible that the market may go down.

Correct

When withdrawing funds, prioritize the oldest investments to minimize tax liabilities (long-term capital gains vs. short-term) and maximize tax efficiency due to compounding.

always withdraw from the oldest investment so it is first in first out meaning whatever you have invested first you will withdraw first not the latest one you will withdraw Because it will reduce your tax the most because you will pay long term capital gains tax and not short term and hopefully if there are consistent or good returns then it will also become the best amount because it would have compounded for the longest time

1 year ago

Correct

When withdrawing funds, prioritize the oldest investments to minimize tax liabilities (long-term capital gains vs. short-term) and maximize tax efficiency due to compounding.

always withdraw from the oldest investment so it is first in first out meaning whatever you have invested first you will withdraw first not the latest one you will withdraw Because it will reduce your tax the most because you will pay long term capital gains tax and not short term and hopefully if there are consistent or good returns then it will also become the best amount because it would have compounded for the longest time

Correct

If Shubham opts for the new tax regime, he should discontinue investing in ELSS.

So, the first thing that I would do is check the tax regime for you and if you are in the new tax regime, if you are in the new tax regime, then stop future ELSS. You don't need to go ahead and buy ELSS.

1 year ago

Correct

If Shubham opts for the new tax regime, he should discontinue investing in ELSS.

So, the first thing that I would do is check the tax regime for you and if you are in the new tax regime, if you are in the new tax regime, then stop future ELSS. You don't need to go ahead and buy ELSS.

Correct

Societal willingness to engage in core human connections like dating, having children, and maintaining friendships will continue to decline due to social media's dopamine effects.

We're not willing to date, not willing to have kids, not willing to have friends, not willing to meet them, not willing to go out of our way to make them feel loved, it's like something fundamental has burst in us, and the truth is it is all the dopamine that social media injects in you.

1 year ago

Incorrect

Societal willingness to engage in core human connections like dating, having children, and maintaining friendships will continue to decline due to social media's dopamine effects.

We're not willing to date, not willing to have kids, not willing to have friends, not willing to meet them, not willing to go out of our way to make them feel loved, it's like something fundamental has burst in us, and the truth is it is all the dopamine that social media injects in you.

Incorrect

Shubham's immediate financial goal should be to build an emergency fund of ₹1 lakh to ₹1.25 lakh.

So, your first goal, in my opinion, should be to create an emergency fund of Rs 1 to 1.25 lakh.

1 year ago

Correct

Shubham's immediate financial goal should be to build an emergency fund of ₹1 lakh to ₹1.25 lakh.

So, your first goal, in my opinion, should be to create an emergency fund of Rs 1 to 1.25 lakh.

Correct

Phones will continue to pull users away from the present moment, the only time they truly have control over.

And your phone takes you in only these two directions One, the truth is there is only one place that can keep you happy Right now There is nothing else in your life, friend, there is no future, there is no past Because you cannot change the past You do not know the future, this is the only time It is truly yours

1 year ago

Correct

Phones will continue to pull users away from the present moment, the only time they truly have control over.

And your phone takes you in only these two directions One, the truth is there is only one place that can keep you happy Right now There is nothing else in your life, friend, there is no future, there is no past Because you cannot change the past You do not know the future, this is the only time It is truly yours

Correct

Shubham should maintain an emergency fund equivalent to 3 to 6 months of his mandatory expenses.

Shubham, at any point you should have three to six times this in the bank for the simple reason that if by chance your income stops, you leave your job or you get laid off or anything else like this, you should have a buffer period of three to six months in which you can still live your life and try to generate income in that.

1 year ago

Correct

Shubham should maintain an emergency fund equivalent to 3 to 6 months of his mandatory expenses.

Shubham, at any point you should have three to six times this in the bank for the simple reason that if by chance your income stops, you leave your job or you get laid off or anything else like this, you should have a buffer period of three to six months in which you can still live your life and try to generate income in that.

Correct

Phones will continue to focus users on past mistakes and regrets, leading to stress and a sense of needing to 'hustle'.

This phone, whether you use it for information, use it for the most positive things, use it to stay away, use it to invest, is your enemy because it takes you in only two directions. Either your history, your past, will take you in one direction or it will take you in the other. To make you realize that you made mistakes To make you realize that if you had worked a little harder, you would have been somewhere else in life To tell you that your mistake, your oversight, is very costly for you Whether it's your portfolio that keeps showing red, or your relationships, or your exes, you have to be stressed, you have to hustle

1 year ago

Correct

Phones will continue to focus users on past mistakes and regrets, leading to stress and a sense of needing to 'hustle'.

This phone, whether you use it for information, use it for the most positive things, use it to stay away, use it to invest, is your enemy because it takes you in only two directions. Either your history, your past, will take you in one direction or it will take you in the other. To make you realize that you made mistakes To make you realize that if you had worked a little harder, you would have been somewhere else in life To tell you that your mistake, your oversight, is very costly for you Whether it's your portfolio that keeps showing red, or your relationships, or your exes, you have to be stressed, you have to hustle

Correct

The total ownership cost of an EV will become equal to a petrol vehicle within three years, after which EVs will be more profitable.

in three years the money will be equal after that only profit

1 year ago

Incorrect

The total ownership cost of an EV will become equal to a petrol vehicle within three years, after which EVs will be more profitable.

in three years the money will be equal after that only profit

Incorrect

Companies will prioritize practical experience and skills over degrees when hiring in the future, rendering degrees less relevant.

Companies will also be like that. If you have that experience, then we are ready to hire you. We don't need any degree because that degree was not helping us anyway.

1 year ago

Correct

Companies will prioritize practical experience and skills over degrees when hiring in the future, rendering degrees less relevant.

Companies will also be like that. If you have that experience, then we are ready to hire you. We don't need any degree because that degree was not helping us anyway.

Correct

Market experiencing a downturn after a period of strong returns, with predictions of further falls.

In the last three years, the market has given blinding returns. Every person feels like a rockstar. Every person feels like they can earn unlimited money in the stock market. But in the last two months, the boat has started sinking. Sanity has started coming. The market is not that strong. Many people are predicting that the market is going to fall even more.

1 year ago

Correct

Market experiencing a downturn after a period of strong returns, with predictions of further falls.

In the last three years, the market has given blinding returns. Every person feels like a rockstar. Every person feels like they can earn unlimited money in the stock market. But in the last two months, the boat has started sinking. Sanity has started coming. The market is not that strong. Many people are predicting that the market is going to fall even more.

Correct

The first loan of Rs. 2 lakh will be repaid by December 2025 by paying an additional Rs. 15,000 per month towards it, in addition to the regular EMI.

from April 2025 onwards you will start your SIP again but this time only of Rs. 000 and there will be three SIPs of Rs. 5000, one will be a SIP of Rs. 00 in Nifty 50 or large cap which you have done now, one SIP of Rs. 000 in flex cap or mid cap which you have done now and one SIP of Rs. 000 in small cap, you will start three SIPs of Rs. 000 and the remaining Rs. 00 months which you have left, you will clear your first loan of Rs. 2 lakh, so only 21 months are left, EMI of Rs. 000 means if you If you pay Rs. 00, you are paying two and a half months' EMI in addition to one month's EMI which is Rs. 000. My calculations roughly say that this entire loan will be repaid in about 10 months or even less than that. So by December 2025, this loan of yours will also be repaid.

1 year ago

Incorrect

The first loan of Rs. 2 lakh will be repaid by December 2025 by paying an additional Rs. 15,000 per month towards it, in addition to the regular EMI.

from April 2025 onwards you will start your SIP again but this time only of Rs. 000 and there will be three SIPs of Rs. 5000, one will be a SIP of Rs. 00 in Nifty 50 or large cap which you have done now, one SIP of Rs. 000 in flex cap or mid cap which you have done now and one SIP of Rs. 000 in small cap, you will start three SIPs of Rs. 000 and the remaining Rs. 00 months which you have left, you will clear your first loan of Rs. 2 lakh, so only 21 months are left, EMI of Rs. 000 means if you If you pay Rs. 00, you are paying two and a half months' EMI in addition to one month's EMI which is Rs. 000. My calculations roughly say that this entire loan will be repaid in about 10 months or even less than that. So by December 2025, this loan of yours will also be repaid.

Incorrect

Build an emergency fund of Rs. 45,000 by stopping current SIPs for five months, which will be available by March 2025.

you have to first build an emergency fund, so here is what I would personally recommend, you have already invested Rs. 9000 of your month in SIP, if you open another bank account with this Rs. 9000, so open one bank account, there is no need to open a new bank account, just open one in the name of your daughter in your current bank account, it is a minor bank account, it will be added very easily, it will be in her name but you will be its custodian and every month as soon as you get your salary, you will stop the SIP of Rs. 9000 right now, so step number one stop all SIPs which are of Rs. 9000, I will say this myself I am saying this but for some reason it is saying end save 00 per month this 00 as soon as you get your salary you will put it in your new bank account auto sweep you cannot touch it it is not your money it is an emergency fund of your family which you will have to create so that if you need money due to any accident you do not have to take any loan again because if you get trapped in more loan then it will be very difficult to get out of it, very difficult you will save this till March 2025 when the EMI or loan of both your phone and laptop gets over then you will save up to March right now it is October so next you will start from November December January February March five months so up to this end you will have 00 in the bank now when March comes things will change

1 year ago

Correct

Build an emergency fund of Rs. 45,000 by stopping current SIPs for five months, which will be available by March 2025.

you have to first build an emergency fund, so here is what I would personally recommend, you have already invested Rs. 9000 of your month in SIP, if you open another bank account with this Rs. 9000, so open one bank account, there is no need to open a new bank account, just open one in the name of your daughter in your current bank account, it is a minor bank account, it will be added very easily, it will be in her name but you will be its custodian and every month as soon as you get your salary, you will stop the SIP of Rs. 9000 right now, so step number one stop all SIPs which are of Rs. 9000, I will say this myself I am saying this but for some reason it is saying end save 00 per month this 00 as soon as you get your salary you will put it in your new bank account auto sweep you cannot touch it it is not your money it is an emergency fund of your family which you will have to create so that if you need money due to any accident you do not have to take any loan again because if you get trapped in more loan then it will be very difficult to get out of it, very difficult you will save this till March 2025 when the EMI or loan of both your phone and laptop gets over then you will save up to March right now it is October so next you will start from November December January February March five months so up to this end you will have 00 in the bank now when March comes things will change

Correct

Invested funds can potentially be utilized to cover future education expenses.

and probably that invested amount will be used for some of your study expenses, at least

1 year ago

Correct

Invested funds can potentially be utilized to cover future education expenses.

and probably that invested amount will be used for some of your study expenses, at least

Correct

Graduates from top, recognized international programs can repay their entire education loans within two to three years of working abroad, with the option to stay longer if desired.

Trust me, if you decide to work there for two to three years, because it's a top program and it's really, really recognized and reputed. You can plan to repay your entire loan and come back within two to three years if you want to come, or you can stay there for a while if you want to stay there.

1 year ago

Correct

Graduates from top, recognized international programs can repay their entire education loans within two to three years of working abroad, with the option to stay longer if desired.

Trust me, if you decide to work there for two to three years, because it's a top program and it's really, really recognized and reputed. You can plan to repay your entire loan and come back within two to three years if you want to come, or you can stay there for a while if you want to stay there.

Correct

A recommended investment strategy involves monthly SIPs of ₹10,000 in Nifty 50, ₹7,000 in a flexi/mid-cap index fund, and ₹4,000 in a small-cap index fund, projecting an annual growth of around ₹18 lakh.

out of this Rs 21,000, you will do an SIP of Rs 1000, not Rs 1000, and that will be in the Nifty 50, Rs 7 lakh in a flexi cap or mid cap index fund and then the remaining Rs 4 lakh in small cap index, which usually grows at around Rs 18 lakh per year.

1 year ago

Incorrect

A recommended investment strategy involves monthly SIPs of ₹10,000 in Nifty 50, ₹7,000 in a flexi/mid-cap index fund, and ₹4,000 in a small-cap index fund, projecting an annual growth of around ₹18 lakh.

out of this Rs 21,000, you will do an SIP of Rs 1000, not Rs 1000, and that will be in the Nifty 50, Rs 7 lakh in a flexi cap or mid cap index fund and then the remaining Rs 4 lakh in small cap index, which usually grows at around Rs 18 lakh per year.

Incorrect

Scholarships and personal loans will become available once admission offers are secured for higher education abroad.

once you get the offer letter, then many avenues will open up. There will be scholarship avenues. You can take out loans. You will be able to take out those loans in your name. And you won't be able to do anything like that.

1 year ago

Correct

Scholarships and personal loans will become available once admission offers are secured for higher education abroad.

once you get the offer letter, then many avenues will open up. There will be scholarship avenues. You can take out loans. You will be able to take out those loans in your name. And you won't be able to do anything like that.

Correct

After selling the house for 26-28 lakh rupees and paying capital gains tax, an estimated 7-9 lakh rupees will be available.

So, I would say that if I am able to get 26 to 28 lakh rupees, then that will be a good amount. After that, you will pay capital gains tax and capital gains tax will be around 10 lakh rupees net. So, the lump sum amount you will have will be around 7 to 9 lakh rupees.

1 year ago

Incorrect

After selling the house for 26-28 lakh rupees and paying capital gains tax, an estimated 7-9 lakh rupees will be available.

So, I would say that if I am able to get 26 to 28 lakh rupees, then that will be a good amount. After that, you will pay capital gains tax and capital gains tax will be around 10 lakh rupees net. So, the lump sum amount you will have will be around 7 to 9 lakh rupees.

Incorrect

A profit of 10 lakh rupees from selling the house is estimated to incur a capital gains tax of approximately 80,000 to 1 lakh rupees.

you will have to pay tax of around 10 lakh rupees on that. Meaning, if you assume that you earn a profit of 10 lakh rupees from the loan, then you will have to pay tax of 80 lakh rupees or one lakh rupees on that.

1 year ago

Correct

A profit of 10 lakh rupees from selling the house is estimated to incur a capital gains tax of approximately 80,000 to 1 lakh rupees.

you will have to pay tax of around 10 lakh rupees on that. Meaning, if you assume that you earn a profit of 10 lakh rupees from the loan, then you will have to pay tax of 80 lakh rupees or one lakh rupees on that.

Correct

Estimated annual cost of health insurance for a 3-5 lakh cover is 10,000 to 12,000 rupees.

So, 10 to 12 thousand rupees will be your health insurance for a 3 to 5 lakh cover.

1 year ago

Correct

Estimated annual cost of health insurance for a 3-5 lakh cover is 10,000 to 12,000 rupees.

So, 10 to 12 thousand rupees will be your health insurance for a 3 to 5 lakh cover.

Correct

Future ability to afford a house or provide a high standard of living is dependent on income growth.

if you keep growing your income get to the point where you will be able to afford a house or provide a good standard of living for your daughter and yourself

1 year ago

Correct

Future ability to afford a house or provide a high standard of living is dependent on income growth.

if you keep growing your income get to the point where you will be able to afford a house or provide a good standard of living for your daughter and yourself

Correct

Eliminate the habit of being excessively frugal by 2025; instead, spend wisely on things that offer long-term savings.

This habit will have to be eliminated by 2025. Spend money wisely. Spend it on things that will create long-term savings for you.

1 year ago

Correct

Eliminate the habit of being excessively frugal by 2025; instead, spend wisely on things that offer long-term savings.

This habit will have to be eliminated by 2025. Spend money wisely. Spend it on things that will create long-term savings for you.

Correct

A phone currently priced at ₹25 lakh will be priced at ₹50 lakh in the future.

After ₹2500000, the price of the phone will be ₹5000000.

1 year ago

Incorrect

A phone currently priced at ₹25 lakh will be priced at ₹50 lakh in the future.

After ₹2500000, the price of the phone will be ₹5000000.

Incorrect

In 2025, always pay credit card bills in full to avoid accumulating interest charges.

In 2025, remove this habit from your life. You don't have to make any payment with minimum amount due. Full payment is always

1 year ago

Correct

In 2025, always pay credit card bills in full to avoid accumulating interest charges.

In 2025, remove this habit from your life. You don't have to make any payment with minimum amount due. Full payment is always

Correct

Avoid taking high-interest, unsecured consumer loans in 2025.

Stop taking bad consumer loans in 2025.

1 year ago

Correct

Avoid taking high-interest, unsecured consumer loans in 2025.

Stop taking bad consumer loans in 2025.

Correct

Shift focus from impressing others with money to impressing them with hard work and dedication in 2025.

In 2025, if you can make a promise to yourself that I am who I am without money On my own Ability, I will try to impress people with my hard work.

1 year ago

Correct

Shift focus from impressing others with money to impressing them with hard work and dedication in 2025.

In 2025, if you can make a promise to yourself that I am who I am without money On my own Ability, I will try to impress people with my hard work.

Correct

Daily 10-minute meditation sessions can gradually lead to the joy of observing one's feelings and thoughts.

not more than 10 minutes of meditation every day because if you meditate for 10 minutes every day, in the beginning, your thoughts will be like, oh, I had to do this too, I had to do that too, I am feeling this, I am itching here, this is happening, etc. etc. But gradually, after the first week, after the second week, after the third week, you will begin to experience the joy of just observing what you are feeling

1 year ago

Correct

Daily 10-minute meditation sessions can gradually lead to the joy of observing one's feelings and thoughts.

not more than 10 minutes of meditation every day because if you meditate for 10 minutes every day, in the beginning, your thoughts will be like, oh, I had to do this too, I had to do that too, I am feeling this, I am itching here, this is happening, etc. etc. But gradually, after the first week, after the second week, after the third week, you will begin to experience the joy of just observing what you are feeling

Correct

Gradually shift wake-up times by small increments (e.g., 10 minutes earlier each week) rather than abrupt changes to build a sustainable habit.

slowly coax your body, lovingly, through a habit, take it to the point where you want to reach, so instead of setting an alarm for 6 am, set it for 7:50 am.

1 year ago

Correct

Gradually shift wake-up times by small increments (e.g., 10 minutes earlier each week) rather than abrupt changes to build a sustainable habit.

slowly coax your body, lovingly, through a habit, take it to the point where you want to reach, so instead of setting an alarm for 6 am, set it for 7:50 am.

Correct

For 45 days, record a one-minute video daily on a consistent topic, looking directly at the camera to improve speaking skills.

Every day, pick up a topic, any topic which will remain the same for the next 45 days. You have to record a video on your phone for one minute on that topic. You have to look the camera in the eye and record a one-minute video.

1 year ago

Correct

For 45 days, record a one-minute video daily on a consistent topic, looking directly at the camera to improve speaking skills.

Every day, pick up a topic, any topic which will remain the same for the next 45 days. You have to record a video on your phone for one minute on that topic. You have to look the camera in the eye and record a one-minute video.

Correct

Engaging in activities where rejection is probable helps develop resilience against failure.

It will train you on how to deal with failure.

1 year ago

Correct

Engaging in activities where rejection is probable helps develop resilience against failure.

It will train you on how to deal with failure.

Correct

Implementing the discussed challenges will lead to a significantly better start to 2025.

If you adopt them, then 2025 will start on a different level.

1 year ago

Correct

Implementing the discussed challenges will lead to a significantly better start to 2025.

If you adopt them, then 2025 will start on a different level.

Correct

A daily 1% compound interest on ₹1 will result in ₹3780 after 1 year, ₹145,000 after 2 years, ₹5,392,000 after 3 years, and ₹20.37 crore after 4 years.

but remember that ₹1 will increase by 1% every day, so at the end of the year you will have around ₹ 3780. At the end of 2 years you will have ₹ 145000. At the end of 3 years you will have ₹ 5392000 and at the end of 4 years by compounding this every day you will have 20 crore 37 lakh rupees.

1 year ago

Incorrect

A daily 1% compound interest on ₹1 will result in ₹3780 after 1 year, ₹145,000 after 2 years, ₹5,392,000 after 3 years, and ₹20.37 crore after 4 years.

but remember that ₹1 will increase by 1% every day, so at the end of the year you will have around ₹ 3780. At the end of 2 years you will have ₹ 145000. At the end of 3 years you will have ₹ 5392000 and at the end of 4 years by compounding this every day you will have 20 crore 37 lakh rupees.

Incorrect

The loan with a 5000 balance will be repaid by allocating 3660 per month, with the repayment expected to take approximately 8 months.

The remaining amount is minus this approximately 3660. This is towards next shortest loan. Now how much is the next shortest loan? This is the 5000 one, how much would be left in it, let's see, 8 months would have passed because these were 6 months, these two months were for repaying other people, so how much do we have towards wastage and how much is left in this? If 800 is left, then how much will we save every month now? If you give this plus 000 then around 8656 means it will be paid off in around 8 months

1 year ago

Correct

The loan with a 5000 balance will be repaid by allocating 3660 per month, with the repayment expected to take approximately 8 months.

The remaining amount is minus this approximately 3660. This is towards next shortest loan. Now how much is the next shortest loan? This is the 5000 one, how much would be left in it, let's see, 8 months would have passed because these were 6 months, these two months were for repaying other people, so how much do we have towards wastage and how much is left in this? If 800 is left, then how much will we save every month now? If you give this plus 000 then around 8656 means it will be paid off in around 8 months

Correct

The strategy is projected to lead to the repayment of all loans, including a 2-year loan and another loan, within approximately 16 months.

This entire journey, where you had a loan of about 2 years and a loan of about 00, you paid it off in 6 months plus two months plus 8 months, so within about 16 months, this 24-month loan

1 year ago

Incorrect

The strategy is projected to lead to the repayment of all loans, including a 2-year loan and another loan, within approximately 16 months.

This entire journey, where you had a loan of about 2 years and a loan of about 00, you paid it off in 6 months plus two months plus 8 months, so within about 16 months, this 24-month loan

Incorrect

An additional payment of 3375 per month will be made towards the second shortest loan, in addition to its regular EMI, aiming to repay it within two months.

The remaining which is 3375, you will pay off the next shortest loan in addition to the EE. So, yours is being done every month. So, which is the second shortest loan, this one of 00, if it is around 1500 then roughly around 18000 is saved. If we do 5000 for 24, then around 00 is saved. You will pay 3375 every month plus 00 you are already paying. So your total is approximately 875 going towards paying this of 4 towards the pending loan of 9k which means whatever was left for the remaining 6 months, Instead of staying for 6 months, it will be repaid in two months. This entire loan will be repaid in two months only.

1 year ago

Incorrect

An additional payment of 3375 per month will be made towards the second shortest loan, in addition to its regular EMI, aiming to repay it within two months.

The remaining which is 3375, you will pay off the next shortest loan in addition to the EE. So, yours is being done every month. So, which is the second shortest loan, this one of 00, if it is around 1500 then roughly around 18000 is saved. If we do 5000 for 24, then around 00 is saved. You will pay 3375 every month plus 00 you are already paying. So your total is approximately 875 going towards paying this of 4 towards the pending loan of 9k which means whatever was left for the remaining 6 months, Instead of staying for 6 months, it will be repaid in two months. This entire loan will be repaid in two months only.

Incorrect

The personal loan with a 5000 principal and 2 years remaining is predicted to be repaid within 2 months by allocating an additional 3375 per month plus the existing 5000 EMI.

In 2 months only. This entire loan will be repaid in two months only.

1 year ago

Incorrect

The personal loan with a 5000 principal and 2 years remaining is predicted to be repaid within 2 months by allocating an additional 3375 per month plus the existing 5000 EMI.

In 2 months only. This entire loan will be repaid in two months only.

Incorrect

Gold investment value reaches ₹170,000 by 2024.

and Majnu's gold ₹ 170000.

1 year ago

Incorrect

Gold investment value reaches ₹170,000 by 2024.

and Majnu's gold ₹ 170000.

Incorrect

Silver investment value reaches ₹100,000 by 2024.

If we talk about 2024, Raja's silver has become worth around ₹1 lakh

1 year ago

Incorrect

Silver investment value reaches ₹100,000 by 2024.

If we talk about 2024, Raja's silver has become worth around ₹1 lakh

Incorrect

Gold investment value reaches ₹75,000 by 2020.

and Majnu's gold is ₹ 75000.

1 year ago

Incorrect

Gold investment value reaches ₹75,000 by 2020.

and Majnu's gold is ₹ 75000.

Incorrect

Silver investment value reaches ₹100,000 by 2020.

By 2020, Raja's silver is ₹1 lakh

1 year ago

Incorrect

Silver investment value reaches ₹100,000 by 2020.

By 2020, Raja's silver is ₹1 lakh

Incorrect

Gold investment value reaches ₹620,000 by 2015.

Majnu's gold has become worth ₹620000.

1 year ago

Incorrect

Gold investment value reaches ₹620,000 by 2015.

Majnu's gold has become worth ₹620000.

Incorrect

Silver investment value reaches ₹80,000 by 2015.

Now Ranjha's silver is worth ₹80000.

1 year ago

Incorrect

Silver investment value reaches ₹80,000 by 2015.

Now Ranjha's silver is worth ₹80000.

Incorrect

Silver investment value reaches ₹44,000 by 2010.

2010: Majnu's gold ₹305 Ranjha's silver ₹44000

1 year ago

Incorrect

Silver investment value reaches ₹44,000 by 2010.

2010: Majnu's gold ₹305 Ranjha's silver ₹44000

Incorrect

Silver investment value reaches ₹135,000 by 2005.

2005: Majnu's gold ₹115000 Raja's silver ₹135000 Silver is winning.

1 year ago

Incorrect

Silver investment value reaches ₹135,000 by 2005.

2005: Majnu's gold ₹115000 Raja's silver ₹135000 Silver is winning.

Incorrect

L&T shares investment expected to grow 208 times from initial investment.

L&T shares of ₹208 times.

1 year ago

Incorrect

L&T shares investment expected to grow 208 times from initial investment.

L&T shares of ₹208 times.

Incorrect

A minimum annual balance of ₹1 lakh is required to be eligible for the HSBC Smart Value Credit Card.

For this, your annual balance should be at least ₹1 lakh.

1 year ago

Correct

A minimum annual balance of ₹1 lakh is required to be eligible for the HSBC Smart Value Credit Card.

For this, your annual balance should be at least ₹1 lakh.

Correct

The projected investment corpus after 5 years is sufficient to repay the 15 lakh interest-free loan from parents.

you will have approximately 63 lakh rupees as an investment Corpus that means you can safely pay your parents the 15 lakh that you owe them

1 year ago

Incorrect

The projected investment corpus after 5 years is sufficient to repay the 15 lakh interest-free loan from parents.

you will have approximately 63 lakh rupees as an investment Corpus that means you can safely pay your parents the 15 lakh that you owe them

Incorrect

Cardholders of the Paytm Bank credit card will receive 12,000 bonus reward points annually if they spend ₹36,000 or more in that year.

You will get 12000 bonus reward points if you spend ₹36000 in a year

1 year ago

Correct

Cardholders of the Paytm Bank credit card will receive 12,000 bonus reward points annually if they spend ₹36,000 or more in that year.

You will get 12000 bonus reward points if you spend ₹36000 in a year

Correct

An investment corpus of approximately 63 lakh rupees is projected after 5 years based on a recommended monthly investment of 72,000 rupees with assumed rates of return.

at the end of five years you will have approximately 63 lakh rupees as an investment Corpus

1 year ago

Incorrect

An investment corpus of approximately 63 lakh rupees is projected after 5 years based on a recommended monthly investment of 72,000 rupees with assumed rates of return.

at the end of five years you will have approximately 63 lakh rupees as an investment Corpus

Incorrect

By converting monthly EMIs to weekly payments over two months, an extra ₹55,150 could be paid towards debt.

At the end of two months or eight weeks, you would have paid around Rs 55,150 extra over and above that EE of Rs 000.

1 year ago

Incorrect

By converting monthly EMIs to weekly payments over two months, an extra ₹55,150 could be paid towards debt.

At the end of two months or eight weeks, you would have paid around Rs 55,150 extra over and above that EE of Rs 000.

Incorrect

An 'investment acceleration challenge' over 8 weeks is projected to result in a total investment of approximately ₹1,15,000, an increase compared to not undertaking the challenge.

if we do it like this, then the total investment you will make is around 1,150, as against if you had not invested, increase 12,000

1 year ago

Incorrect

An 'investment acceleration challenge' over 8 weeks is projected to result in a total investment of approximately ₹1,15,000, an increase compared to not undertaking the challenge.

if we do it like this, then the total investment you will make is around 1,150, as against if you had not invested, increase 12,000

Incorrect

The speaker suggests that the gold loan can be repaid in approximately 20 months, either through increased payments or a lump sum.

in about 20 months this gold loan will also be repaid completely

1 year ago

Correct

The speaker suggests that the gold loan can be repaid in approximately 20 months, either through increased payments or a lump sum.

in about 20 months this gold loan will also be repaid completely

Correct

New holders of the SBI Simply Save Credit Card will receive 2000 bonus reward points, valued at ₹500, if they activate the card and make purchases within the first 60 days.

2000 bonus reward points which are worth ₹5000000 within the first 60 days of card activation.

1 year ago

Incorrect

New holders of the SBI Simply Save Credit Card will receive 2000 bonus reward points, valued at ₹500, if they activate the card and make purchases within the first 60 days.

2000 bonus reward points which are worth ₹5000000 within the first 60 days of card activation.

Incorrect

A ₹10,000 SIP is predicted to grow to approximately ₹1 lakh in 5 years.

A SIP of ₹10000 will become around ₹1 lakh after 5 years

1 year ago

Correct

A ₹10,000 SIP is predicted to grow to approximately ₹1 lakh in 5 years.

A SIP of ₹10000 will become around ₹1 lakh after 5 years

Correct

A credit card loan with a 6% monthly interest rate will continuously increase and never decrease.

if it is so, then it is important to understand that your amount will always keep increasing, it will never decrease.

1 year ago

Incorrect

A credit card loan with a 6% monthly interest rate will continuously increase and never decrease.

if it is so, then it is important to understand that your amount will always keep increasing, it will never decrease.

Incorrect

A credit card loan with a 5% monthly interest rate will never be repaid, even if minimum payments are made.

if by chance you have taken such a credit card whose interest charge is 5% per month which is the equivalent of how much they charge you the minimum amount due, then your loan will never be repaid

1 year ago

Correct

A credit card loan with a 5% monthly interest rate will never be repaid, even if minimum payments are made.

if by chance you have taken such a credit card whose interest charge is 5% per month which is the equivalent of how much they charge you the minimum amount due, then your loan will never be repaid

Correct

The annual fee for the SBI Simply Save Credit Card is waived if the cardholder spends over ₹1 lakh in a year.

Annual fee waiver: If you spend more than ₹1 lakh, the annual fee of ₹99 will be waived.

1 year ago

Correct

The annual fee for the SBI Simply Save Credit Card is waived if the cardholder spends over ₹1 lakh in a year.

Annual fee waiver: If you spend more than ₹1 lakh, the annual fee of ₹99 will be waived.

Correct

A Rs 50,000 credit card debt will take 17 years to repay with a 4% monthly interest rate.

9 years to repay ₹3000000, if the interest is 4 per month, then to repay the same ₹5000000, it will take 17 years, 8 years and almost double, this is the difference of just 1 per

1 year ago

Incorrect

A Rs 50,000 credit card debt will take 17 years to repay with a 4% monthly interest rate.

9 years to repay ₹3000000, if the interest is 4 per month, then to repay the same ₹5000000, it will take 17 years, 8 years and almost double, this is the difference of just 1 per

Incorrect

A ₹50,000 credit card debt will take 9 years to repay if paying the minimum amount due and the interest rate is 3% per month.

9 years, during that time you would have paid 90000 to repay this 50000

1 year ago

Incorrect

A ₹50,000 credit card debt will take 9 years to repay if paying the minimum amount due and the interest rate is 3% per month.

9 years, during that time you would have paid 90000 to repay this 50000

Incorrect

A Rs 30,000 credit card debt will take 9 years to repay with a 3% monthly interest rate.

9 years to repay ₹3000000, if the interest is 4 per month, then to repay the same ₹5000000, it will take 17 years, 8 years and almost double, this is the difference of just 1 per

1 year ago

Incorrect

A Rs 30,000 credit card debt will take 9 years to repay with a 3% monthly interest rate.

9 years to repay ₹3000000, if the interest is 4 per month, then to repay the same ₹5000000, it will take 17 years, 8 years and almost double, this is the difference of just 1 per

Incorrect

Repaying a Rs 50,000 credit card debt by only paying the minimum amount will take 110 months.

in fact it will take 110 months to repay this loan of 50000 if you keep paying the minimum amount for 9 years

1 year ago

Incorrect

Repaying a Rs 50,000 credit card debt by only paying the minimum amount will take 110 months.

in fact it will take 110 months to repay this loan of 50000 if you keep paying the minimum amount for 9 years

Incorrect

The ideal financial management approach for partners involves pooling a significant portion of income for shared expenses and investments, while retaining a smaller amount for individual 'play money' or personal discretionary spending.

What it means is partner one and partner two both have salary bank accounts and both of them will say that we will keep Rs. 10, 15, 20 or whatever is there from this for ourselves and the rest will be swapped in to the common bank account. So that Rs. 10, 20 becomes your individual fund money, play money. You can use it in any form, but it is not your investment amount. It is, as I said, your fun money and your play money. So, from the common pool, you will spend your monthly expenses. From that, you will spend for your needs, from that, for your desires and from that, for your investments.

1 year ago

Correct

The ideal financial management approach for partners involves pooling a significant portion of income for shared expenses and investments, while retaining a smaller amount for individual 'play money' or personal discretionary spending.

What it means is partner one and partner two both have salary bank accounts and both of them will say that we will keep Rs. 10, 15, 20 or whatever is there from this for ourselves and the rest will be swapped in to the common bank account. So that Rs. 10, 20 becomes your individual fund money, play money. You can use it in any form, but it is not your investment amount. It is, as I said, your fun money and your play money. So, from the common pool, you will spend your monthly expenses. From that, you will spend for your needs, from that, for your desires and from that, for your investments.

Correct

It is advisable to maintain a professional distance and avoid lending significant amounts of money to colleagues and acquaintances. Small amounts for items like tea or snacks are an exception.

Never give them any money. You will always maintain a professional distance. So, in your office, if your colleagues, who are not your friends, ask for money, you should say very clearly that friend, in a professional setting, I am not comfortable lending or borrowing money, so I am really sorry, I will not be able to help, of course, it depends on the amount because if someone is asking for Rs. 10-20 for a samosa or tea. You will give it again don't expect it back if it comes then it's great but if someone is suddenly asking for 5000 10000 50000 then you will put your foot down and say sorry in a professional setting neither do I ask for money from anyone nor do I give money to anyone because I feel that that is a clean way of doing it

1 year ago

Correct

It is advisable to maintain a professional distance and avoid lending significant amounts of money to colleagues and acquaintances. Small amounts for items like tea or snacks are an exception.

Never give them any money. You will always maintain a professional distance. So, in your office, if your colleagues, who are not your friends, ask for money, you should say very clearly that friend, in a professional setting, I am not comfortable lending or borrowing money, so I am really sorry, I will not be able to help, of course, it depends on the amount because if someone is asking for Rs. 10-20 for a samosa or tea. You will give it again don't expect it back if it comes then it's great but if someone is suddenly asking for 5000 10000 50000 then you will put your foot down and say sorry in a professional setting neither do I ask for money from anyone nor do I give money to anyone because I feel that that is a clean way of doing it

Correct

Children should focus on their own investments until age 30 and only contribute to their parents' income in cases of genuine need or difficult times.

Don't think about giving back to them. Family because it is expected that your parents will still be in working age, so they are earning for them, so they can take care of themselves. If it is a difficult time or there is a great need, of course, help them. This is without thought. But if they don't need that help, then the first saddle we normally leave with our mother, saying, 'Mom, this is my first salary, it is yours. That is what we all should do.' But after that, my suggestion is, for 30 years, there is no need to contribute towards your parents' income.

1 year ago

Correct

Children should focus on their own investments until age 30 and only contribute to their parents' income in cases of genuine need or difficult times.

Don't think about giving back to them. Family because it is expected that your parents will still be in working age, so they are earning for them, so they can take care of themselves. If it is a difficult time or there is a great need, of course, help them. This is without thought. But if they don't need that help, then the first saddle we normally leave with our mother, saying, 'Mom, this is my first salary, it is yours. That is what we all should do.' But after that, my suggestion is, for 30 years, there is no need to contribute towards your parents' income.

Correct

An investment of 50 lakhs grew to 10 crores within four years.

recently I made a video where an investment of 50 lakhs has now become 10 crores in a matter of four years

1 year ago

Incorrect

An investment of 50 lakhs grew to 10 crores within four years.

recently I made a video where an investment of 50 lakhs has now become 10 crores in a matter of four years

Incorrect

The speaker has invested in Solana and expects a potential 5x return on this portion of their investment.

I bought one Bitcoin, 10 Ethereus, 100 Solana, and I've bought them and they're just sitting there. I don't buy more than that, nor do I ever intend to sell them. I'm patiently watching where it goes. If it becomes 5%, it becomes 5%.

1 year ago

Incorrect

The speaker has invested in Solana and expects a potential 5x return on this portion of their investment.

I bought one Bitcoin, 10 Ethereus, 100 Solana, and I've bought them and they're just sitting there. I don't buy more than that, nor do I ever intend to sell them. I'm patiently watching where it goes. If it becomes 5%, it becomes 5%.

Incorrect

The speaker has invested in Ethereum and expects a potential 5x return on this portion of their investment.

I bought one Bitcoin, 10 Ethereus, 100 Solana, and I've bought them and they're just sitting there. I don't buy more than that, nor do I ever intend to sell them. I'm patiently watching where it goes. If it becomes 5%, it becomes 5%.

1 year ago

Incorrect

The speaker has invested in Ethereum and expects a potential 5x return on this portion of their investment.

I bought one Bitcoin, 10 Ethereus, 100 Solana, and I've bought them and they're just sitting there. I don't buy more than that, nor do I ever intend to sell them. I'm patiently watching where it goes. If it becomes 5%, it becomes 5%.

Incorrect

The speaker has invested in Bitcoin and expects a potential 5x return on this portion of their investment.

I bought one Bitcoin, 10 Ethereus, 100 Solana, and I've bought them and they're just sitting there. I don't buy more than that, nor do I ever intend to sell them. I'm patiently watching where it goes. If it becomes 5%, it becomes 5%.

1 year ago

Incorrect

The speaker has invested in Bitcoin and expects a potential 5x return on this portion of their investment.

I bought one Bitcoin, 10 Ethereus, 100 Solana, and I've bought them and they're just sitting there. I don't buy more than that, nor do I ever intend to sell them. I'm patiently watching where it goes. If it becomes 5%, it becomes 5%.

Incorrect

Allocate 50% of available funds to a small-cap mutual fund.

and then about 50% will be in the small-cap mutual fund.

1 year ago

Correct

Allocate 50% of available funds to a small-cap mutual fund.

and then about 50% will be in the small-cap mutual fund.

Correct

The equity portion of the portfolio, invested in the TSX, is expected to yield around 8.5% annually.

that will earn us at around 85k the equivalent of what is the Indian stock market now

1 year ago

Correct

The equity portion of the portfolio, invested in the TSX, is expected to yield around 8.5% annually.

that will earn us at around 85k the equivalent of what is the Indian stock market now

Correct

The medium-risk segment of the portfolio, a combination of GIC and T&Cs (likely referring to traditional investments), is expected to yield around 6.5% annually.

Around 6 and a half per and so and that I think is reasonable

1 year ago

Correct

The medium-risk segment of the portfolio, a combination of GIC and T&Cs (likely referring to traditional investments), is expected to yield around 6.5% annually.

Around 6 and a half per and so and that I think is reasonable

Correct

The low-risk segment of the portfolio, invested in a long-term GIC, is expected to yield an average return of 4.5%.

If we get a 4.5 on an average return, okay? Then the remaining 50 rupees, we will put in what you have right now.

1 year ago

Correct

The low-risk segment of the portfolio, invested in a long-term GIC, is expected to yield an average return of 4.5%.

If we get a 4.5 on an average return, okay? Then the remaining 50 rupees, we will put in what you have right now.

Correct

The projected investment corpus after 5 years is 3.9 crore INR.

after 5 years, you will have a total investment corpus of approximately Rs 3 crore 90 lakh.

1 year ago

Incorrect

The projected investment corpus after 5 years is 3.9 crore INR.

after 5 years, you will have a total investment corpus of approximately Rs 3 crore 90 lakh.

Incorrect

The combined annual growth rate from stock market appreciation (8-9%) and currency appreciation (3%) is projected to be around 11-12%.

So, if you take stock market appreciation at 8% to 9% and currency appreciation at around 3%, you're around 11% to 12%.

1 year ago

Incorrect

The combined annual growth rate from stock market appreciation (8-9%) and currency appreciation (3%) is projected to be around 11-12%.

So, if you take stock market appreciation at 8% to 9% and currency appreciation at around 3%, you're around 11% to 12%.

Incorrect

Allocate 1.5% of available funds to a Nifty 50 mutual fund.

So, next 1.5% will be in the Nifty 50 mutual fund

1 year ago

Correct

Allocate 1.5% of available funds to a Nifty 50 mutual fund.

So, next 1.5% will be in the Nifty 50 mutual fund

Correct

Small-cap mutual funds are highly susceptible to market volatility and will be the first to crash during economic instability or regulatory changes.

Small-cap companies in the stock market experience the most fluctuations because they are small by definition. So, if there is any economic derailment, any taxation issue, any regulation, any dollar-euro or anything else fluctuates, the small-cap industry is the first to start shaking and crashes because of that.

1 year ago

Incorrect

Small-cap mutual funds are highly susceptible to market volatility and will be the first to crash during economic instability or regulatory changes.

Small-cap companies in the stock market experience the most fluctuations because they are small by definition. So, if there is any economic derailment, any taxation issue, any regulation, any dollar-euro or anything else fluctuates, the small-cap industry is the first to start shaking and crashes because of that.

Incorrect

The investment corpus is projected to grow to INR 1.44 crore in 5 years, based on an initial investment of approximately INR 91 lakh.

So that 90 lakh per year will be around Rs 1 crore 44 lakh.

1 year ago

Incorrect

The investment corpus is projected to grow to INR 1.44 crore in 5 years, based on an initial investment of approximately INR 91 lakh.

So that 90 lakh per year will be around Rs 1 crore 44 lakh.

Incorrect

Extend the loan repayment period for a two-wheeler from 1.5 years to 2 or 3 years to reduce monthly EMI payments.

Instead of taking a loan of one and a half years, I will take a loan of two or three years so that the EMI of my bank loan gets covered within one and a half or two rupees.

1 year ago

Correct

Extend the loan repayment period for a two-wheeler from 1.5 years to 2 or 3 years to reduce monthly EMI payments.

Instead of taking a loan of one and a half years, I will take a loan of two or three years so that the EMI of my bank loan gets covered within one and a half or two rupees.

Correct

Allocate Rs. 1000-1500 monthly for the next year towards learning new skills to enhance income potential.

Every month you have to spend Rs. 1000 on learning new skills

1 year ago

Correct

Allocate Rs. 1000-1500 monthly for the next year towards learning new skills to enhance income potential.

Every month you have to spend Rs. 1000 on learning new skills

Correct

Within the next 1-2 months, an individual should aim to secure health insurance for their mother.

in the next one or two months, you should be in a position where you can take health insurance for your mother as well.

1 year ago

Incorrect

Within the next 1-2 months, an individual should aim to secure health insurance for their mother.

in the next one or two months, you should be in a position where you can take health insurance for your mother as well.

Incorrect

Total estimated cost for children's university fees over the next three years is CAD 40,000.

So I will be safe to assume that I will need around ₹0,000

1 year ago

Correct

Total estimated cost for children's university fees over the next three years is CAD 40,000.

So I will be safe to assume that I will need around ₹0,000

Correct

By optimizing bike purchase and loan terms, an individual can save approximately Rs. 3000-5000 per month.

this means you will save around 3000 per month

1 year ago

Incorrect

By optimizing bike purchase and loan terms, an individual can save approximately Rs. 3000-5000 per month.

this means you will save around 3000 per month

Incorrect

Estimated annual cost for both children's university expenses is CAD 10,000.

dono ka mila ke 10000 ok and this will be per year ok later so it will be safe

1 year ago

Incorrect

Estimated annual cost for both children's university expenses is CAD 10,000.

dono ka mila ke 10000 ok and this will be per year ok later so it will be safe

Incorrect

By opting for a used bike and a longer loan term (36 months instead of 18), the monthly EMI for a Rs. 70,000 loan can be reduced from potentially Rs. 4000-5000 to Rs. 1300.

if you make only these two changes then the EMI which you were planning of 4000 or 5000 right now will come to 13,000.

1 year ago

Correct

By opting for a used bike and a longer loan term (36 months instead of 18), the monthly EMI for a Rs. 70,000 loan can be reduced from potentially Rs. 4000-5000 to Rs. 1300.

if you make only these two changes then the EMI which you were planning of 4000 or 5000 right now will come to 13,000.

Correct

The total expenditure for a 3kW solar panel system will be recovered through savings in 3.5 years.

your entire expenditure will be recovered within 35 years.

1 year ago

Incorrect

The total expenditure for a 3kW solar panel system will be recovered through savings in 3.5 years.

your entire expenditure will be recovered within 35 years.

Incorrect

Speaker believes the tax on capital gains will increase to 20% or potentially higher in the near future, citing government predictions and budget.

But as per the budget and the government's predictions, I am of the believe that it will go to 20 or maybe even more than that.

1 year ago

Incorrect

Speaker believes the tax on capital gains will increase to 20% or potentially higher in the near future, citing government predictions and budget.

But as per the budget and the government's predictions, I am of the believe that it will go to 20 or maybe even more than that.

Incorrect

The government may increase capital gains tax to 30% in the long term.

but there is a strong possibility that the government wants to make it at 30

1 year ago

Incorrect

The government may increase capital gains tax to 30% in the long term.

but there is a strong possibility that the government wants to make it at 30

Incorrect

The small-cap market is expected to experience a significant correction due to its high valuation.

where small cap is definitely going to correct a lot because it has become very highly valued.

1 year ago

Incorrect

The small-cap market is expected to experience a significant correction due to its high valuation.

where small cap is definitely going to correct a lot because it has become very highly valued.

Incorrect

The stock market is currently considered 'hot', and a correction is anticipated within the next year.

And the market is very hot right now, so correction is quite possible in the next year.

1 year ago

Correct

The stock market is currently considered 'hot', and a correction is anticipated within the next year.

And the market is very hot right now, so correction is quite possible in the next year.

Correct

An SIP of ₹25,000 per month, continued for 9 years, is projected to yield approximately ₹1.10 crore.

If you wait for 9 years, the value of your investment will be 1 crore 10 lakhs.

1 year ago

Incorrect

An SIP of ₹25,000 per month, continued for 9 years, is projected to yield approximately ₹1.10 crore.

If you wait for 9 years, the value of your investment will be 1 crore 10 lakhs.

Incorrect

A portfolio of Rs. 8.87 crore growing at 12% annual return will generate an additional Rs. 1 crore in the following year (without further investment).

If the same amount grows every year from Rs 12, my rate of return is quite high because I have taken some aggressive bets, but that's a different story if that If 12% also grows, then ext year without adding anything next year without adding anything I will have Rs 1 crore more because 12% of 88.7 is greater than 1 crore

1 year ago

Correct

A portfolio of Rs. 8.87 crore growing at 12% annual return will generate an additional Rs. 1 crore in the following year (without further investment).

If the same amount grows every year from Rs 12, my rate of return is quite high because I have taken some aggressive bets, but that's a different story if that If 12% also grows, then ext year without adding anything next year without adding anything I will have Rs 1 crore more because 12% of 88.7 is greater than 1 crore

Correct

Rs. 10 lakh invested at a 6% annual return (FD rate) will grow to Rs. 34 lakh.

If we invest the same at ₹8 lakh, then if we invest it at ₹6 instead of ₹12, which is the fixed deposit rate, then we will take that ₹10 lakh to just ₹34 lakh.

1 year ago

Correct

Rs. 10 lakh invested at a 6% annual return (FD rate) will grow to Rs. 34 lakh.

If we invest the same at ₹8 lakh, then if we invest it at ₹6 instead of ₹12, which is the fixed deposit rate, then we will take that ₹10 lakh to just ₹34 lakh.

Correct

The speaker estimates a monthly EMI of around Rs. 8050 for a home loan of Rs. 13 lakh taken for 20 years at an interest rate of 8.5%. He believes Arindam will be able to afford this within two years.

If we take it for 20 years, your monthly EMI will be Rs 80. If you take it for 25 years, it will be Rs 10,470... My suggestion would be that you start from 20 years because after two years, you will have your savings potential. Keeping that in mind, I am hoping that within two years you will be able to afford this EMI of Rs 80

1 year ago

Incorrect

The speaker estimates a monthly EMI of around Rs. 8050 for a home loan of Rs. 13 lakh taken for 20 years at an interest rate of 8.5%. He believes Arindam will be able to afford this within two years.

If we take it for 20 years, your monthly EMI will be Rs 80. If you take it for 25 years, it will be Rs 10,470... My suggestion would be that you start from 20 years because after two years, you will have your savings potential. Keeping that in mind, I am hoping that within two years you will be able to afford this EMI of Rs 80

Incorrect

For a house worth Rs. 95 lakhs, a loan of Rs. 70-73 lakhs would result in a monthly EMI of approximately Rs. 57,000.

But if we can estimate and the value of the house is around 95 lakhs, then you will have to take a loan of around 70-73 lakhs and its EMI will be around 57,000 per month.

1 year ago

Correct

For a house worth Rs. 95 lakhs, a loan of Rs. 70-73 lakhs would result in a monthly EMI of approximately Rs. 57,000.

But if we can estimate and the value of the house is around 95 lakhs, then you will have to take a loan of around 70-73 lakhs and its EMI will be around 57,000 per month.

Correct

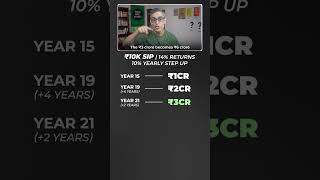

An investment of 5000 with a 10% annual step-up is projected to yield 4 crore 17 lakh annually.

invest 5000 % return and annual step up of 10% will give you 4 crore 17 lakh

1 year ago

Incorrect

An investment of 5000 with a 10% annual step-up is projected to yield 4 crore 17 lakh annually.

invest 5000 % return and annual step up of 10% will give you 4 crore 17 lakh

Incorrect

A health insurance cover of ₹2-5 lakh for the individual and her son is recommended, with an estimated annual cost of ₹700-1000 per month.

And I think if you take a cover of Rs. 2 to ₹ lakh because you are still young, the chances of hospitalization are lower. This should be a cover of Rs. 2 to ₹ lakh. This will not be very expensive on a yearly basis... my first suggestion would be let's go with a 000 per month health insurance plan of roughly 1 to 700 rupees. Let's assume it will be 700 rupees.

1 year ago

Correct

A health insurance cover of ₹2-5 lakh for the individual and her son is recommended, with an estimated annual cost of ₹700-1000 per month.

And I think if you take a cover of Rs. 2 to ₹ lakh because you are still young, the chances of hospitalization are lower. This should be a cover of Rs. 2 to ₹ lakh. This will not be very expensive on a yearly basis... my first suggestion would be let's go with a 000 per month health insurance plan of roughly 1 to 700 rupees. Let's assume it will be 700 rupees.

Correct

A life insurance cover of ₹50 lakh can be obtained for approximately ₹700-800 per month, covering the individual until age 60.

If you take a cover of Rs 50 lakh, it means in the event of death of the son and the nominee will get Rs 50 lakh and its approximate cost will be around Rs 7 to 800 per month and in 60 years

1 year ago

Correct

A life insurance cover of ₹50 lakh can be obtained for approximately ₹700-800 per month, covering the individual until age 60.

If you take a cover of Rs 50 lakh, it means in the event of death of the son and the nominee will get Rs 50 lakh and its approximate cost will be around Rs 7 to 800 per month and in 60 years

Correct

Consistent investment without increasing the amount will lead to a corpus of approximately ₹13 lakh in 5 years.

After five years, the total of all these investments will come to 13 lakhs, approximately ₹1 lakh.

1 year ago

Incorrect

Consistent investment without increasing the amount will lead to a corpus of approximately ₹13 lakh in 5 years.

After five years, the total of all these investments will come to 13 lakhs, approximately ₹1 lakh.

Incorrect

Following the previous growth, the subsequent Rs. 50 lakh will be added in 3 years.

The next Rs. 50 lakh will come in just 3 years.

1 year ago

Incorrect

Following the previous growth, the subsequent Rs. 50 lakh will be added in 3 years.

The next Rs. 50 lakh will come in just 3 years.

Incorrect

After the initial Rs. 1 lakh is accumulated, the next Rs. 50 lakh will be added in 5 years.

But the next Rs. 50 lakh will come in just 5 years.

1 year ago

Incorrect

After the initial Rs. 1 lakh is accumulated, the next Rs. 50 lakh will be added in 5 years.

But the next Rs. 50 lakh will come in just 5 years.

Incorrect

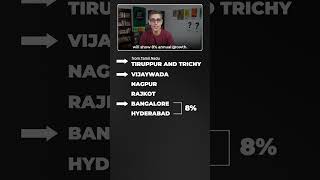

Surat is predicted to be the number one fastest growing city.

Surat is at number one.

1 year ago

Correct

Surat is predicted to be the number one fastest growing city.

Surat is at number one.

Correct

Bangalore and Hyderabad are predicted to experience approximately 8% annual growth.

Talking about big cities, Bangalore and Hyderabad will show annual growth at around 8%.

1 year ago

Correct

Bangalore and Hyderabad are predicted to experience approximately 8% annual growth.

Talking about big cities, Bangalore and Hyderabad will show annual growth at around 8%.

Correct

iPhone 7 price to depreciate to ₹00 in 5 years.

iPhone 7. After that, the price of the phone would be around ₹00.

1 year ago

Incorrect

iPhone 7 price to depreciate to ₹00 in 5 years.

iPhone 7. After that, the price of the phone would be around ₹00.

Incorrect

Investing in the stock market for 1 year has a 50-50 chance of earning money, indicating high risk.

if you invest for one year, what is the guarantee that you will earn money 5050, which is a coin toss, so it is very risky

1 year ago

Correct

Investing in the stock market for 1 year has a 50-50 chance of earning money, indicating high risk.

if you invest for one year, what is the guarantee that you will earn money 5050, which is a coin toss, so it is very risky

Correct

Investing in the stock market for 3 years offers a 90% guarantee of profitable returns.

if you invest for 3 years, what is the guarantee that you will earn profitable returns or positive returns 90%

1 year ago

Incorrect

Investing in the stock market for 3 years offers a 90% guarantee of profitable returns.

if you invest for 3 years, what is the guarantee that you will earn profitable returns or positive returns 90%

Incorrect

Life insurance premiums will increase upon reaching ages 30 and 35.

As soon as you turn 30, the premium increases. As soon as you turn 35, the premium increases and then it becomes a number six.

1 year ago

Correct

Life insurance premiums will increase upon reaching ages 30 and 35.

As soon as you turn 30, the premium increases. As soon as you turn 35, the premium increases and then it becomes a number six.

Correct

Investing in small caps carries a risk of 40-50% decrease in value within 1-2 years.

If you invest in small caps, it is so risky that in a year or two, your money can decrease by 40-50%, it can increase.

1 year ago

Correct

Investing in small caps carries a risk of 40-50% decrease in value within 1-2 years.

If you invest in small caps, it is so risky that in a year or two, your money can decrease by 40-50%, it can increase.

Correct

The speaker predicts a potential correction in the small-cap stock market within the next 1-2 years.

And in my opinion too, there may be a correction in the next one or two years.

1 year ago

Correct

The speaker predicts a potential correction in the small-cap stock market within the next 1-2 years.

And in my opinion too, there may be a correction in the next one or two years.

Correct

The speaker predicts that ₹7 lakh can be saved for the parents within one year through investments, which could cover their lifetime expenses if they are frugal.

if in a year itself they, like no baba, say that Gaurav, enough Now I think I want to stop working, then in that year you will have saved seven lakh rupees for them through this investment

1 year ago

Incorrect

The speaker predicts that ₹7 lakh can be saved for the parents within one year through investments, which could cover their lifetime expenses if they are frugal.

if in a year itself they, like no baba, say that Gaurav, enough Now I think I want to stop working, then in that year you will have saved seven lakh rupees for them through this investment

Incorrect

Aspen should prioritize paying off a 50,000 personal loan by October 2024.

First of all, pay off the personal loan of Rs 50000 by October 24.

1 year ago

Correct

Aspen should prioritize paying off a 50,000 personal loan by October 2024.

First of all, pay off the personal loan of Rs 50000 by October 24.

Correct

An SIP of Rs. 5000 per year with a 10% step-up and 15% return will result in Rs. 10 lakh within 11 years.

within 11 years Rs. lakh

1 year ago

Correct

An SIP of Rs. 5000 per year with a 10% step-up and 15% return will result in Rs. 10 lakh within 11 years.

within 11 years Rs. lakh

Correct

An SIP of Rs. 5000 per year with a 10% step-up and 15% return will result in Rs. 10 lakh within 7 years.

within 7 years you will have Rs. lakh

1 year ago

Incorrect

An SIP of Rs. 5000 per year with a 10% step-up and 15% return will result in Rs. 10 lakh within 7 years.

within 7 years you will have Rs. lakh

Incorrect

Aspen plans to start an Executive MBA within two years, after clearing their study loan.

I will prepare for MBA only when my study loan gets cleared, first of all I am planning to do it by the end of this year and I want to clear it by July next year, so I am planning that as soon as that gets over within the next two years, I have thought of going for MBA.

1 year ago

Incorrect

Aspen plans to start an Executive MBA within two years, after clearing their study loan.

I will prepare for MBA only when my study loan gets cleared, first of all I am planning to do it by the end of this year and I want to clear it by July next year, so I am planning that as soon as that gets over within the next two years, I have thought of going for MBA.

Incorrect

With a higher monthly SIP amount leading to a corpus of ₹1.16 crore, a ₹75,000 monthly withdrawal from a Nifty 50 index fund can last a lifetime.

If we need Rs. 75,000 per month, you will see it will last. The power will never end.

1 year ago

Incorrect

With a higher monthly SIP amount leading to a corpus of ₹1.16 crore, a ₹75,000 monthly withdrawal from a Nifty 50 index fund can last a lifetime.

If we need Rs. 75,000 per month, you will see it will last. The power will never end.

Incorrect

An initial investment of 1.5 crore, with a 10% annual increase, will grow to 3 crore 30 lakh.

then this 1.5 crore will become 3 crore 30 lakh

1 year ago

Incorrect

An initial investment of 1.5 crore, with a 10% annual increase, will grow to 3 crore 30 lakh.

then this 1.5 crore will become 3 crore 30 lakh

Incorrect

Net of tax returns should be higher than 6%.

The net of tax, which means the return after taxation, should be higher than 6%.

1 year ago

Incorrect

Net of tax returns should be higher than 6%.

The net of tax, which means the return after taxation, should be higher than 6%.

Incorrect

A monthly withdrawal of ₹75,000 from a ₹77.7 lakh corpus (generated from Nifty 50 index fund) will be exhausted by age 61.

And if you need Rs. 75,000, this amount will be exhausted at the age of 61.

1 year ago

Incorrect

A monthly withdrawal of ₹75,000 from a ₹77.7 lakh corpus (generated from Nifty 50 index fund) will be exhausted by age 61.

And if you need Rs. 75,000, this amount will be exhausted at the age of 61.

Incorrect

A corpus of approximately ₹77.7 lakh, generated from a Nifty 50 index fund, can sustain a monthly withdrawal of ₹50,000 (increasing with inflation) throughout a lifetime, assuming a 13% NAV growth and capital gains tax considerations.

At the age of 45, you have Rs 7.7 million. Okay, and you have 66617 units. Now, to generate this Rs 50,000 every month, you will have to start selling these units. This is the way you will work. ... Meaning, this amount will keep giving you Rs. 50,000 per month throughout your life, increasing with inflation at that point.

1 year ago

Incorrect

A corpus of approximately ₹77.7 lakh, generated from a Nifty 50 index fund, can sustain a monthly withdrawal of ₹50,000 (increasing with inflation) throughout a lifetime, assuming a 13% NAV growth and capital gains tax considerations.